This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The most common mistake Howe sees planners make is that they don’t read their contracts. Contracts are self-inflicted wounds,” he says. You have no rights or responsibilities unless they are in the contract.” You can’t insure against everything. Do Your Homework. The best practice is to instead have a back-up plan.”

Establishing the conference fee, contracting with the venue and locking the dates will require some effort. By offering refund insurance at a nominal rate, you can give each person peace of mind that they’ll receive their registration fee back in the case of an emergency. Sell refund protection.

Even months after a disaster, even if the reality on the ground is actually pretty good, your prospective attendees, exhibitors, and sponsors may still be holding onto negative perceptions that will keep them from wanting to attend. Analyze your insurance coverage. Poll your stakeholders. Will it be safe?

Venue Contracts. Venue contracts will also look much different than they did pre-COVID. Make sure to read your contract carefully and ask any questions of the on-site team so you know all of your options. Event Insurance. This can include cancellation or postponement policies, and even COVID liabilities. Safety Guide.

The rent-to-own contract also includes the purchase price of the home. There are fees, negotiable purchase contracts, and other considerations you should keep in mind (and ask about) when considering a rent-to-own option. Before you sign the contract, you already know what you’ll spend on the property at the end of the lease term.

It’s also important for prospective event planners to understand that while the field can be financially rewarding, it can also be demanding and stressful. They are often employed by the company itself, or by an external planning organization that contracts with their clients. Learn how to negotiate contracts.

Equipment rental and related costs Licences and permits Insurance costs Establish your event team. Create a shortlist and negotiate with talents Create written contracts (make sure not to miss any details) Secure promotional details (bio, headshot, session draft, etc.) sharing the event on their social networks) Finalize paperwork.

ESPONDA: In the beginning, it was popular for visitors to have insurance and many hotels also offered this option. But many hotels and resorts and villa companies are cooperating by offering at least a 50 percent discount if the guest does not have insurance. Who pays for that?

For example, you need to procure the right insurance to protect your brand, your team, and your clients. Do you have an ironclad contract ready to go? Added elements like lighting, furniture rentals, or floral design can up the ante with prospective clients. How much staffing will you need to get started?

Florida’s unique weather patterns, flood zones, and homeowner’s insurance requirements can add extra considerations to the homebuying process. They can also help with essential tasks such as scheduling inspections, reviewing contracts, and arranging for the sale’s closing.

Whether you can serve alcohol, accessibility concerns, whether you’ll need to get additional insurance, can you bring your own catering, etc. Sign contract with venue and vendors. If possible, have contracts finalized and signed. Finalize sponsor contracts and details. Negotiate details with the venue. Sponsorship.

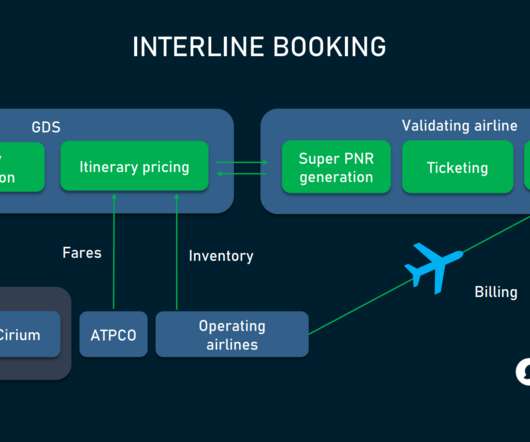

However, the contract doesn’t cover all nuances of interlining, so many other things have to be formalized separately. Other factors also prevent carriers from understanding their financial prospects. It can be a travel insurance voucher or a coverage offered by the platform provider. Bilateral agreements.

This information may include your credit report with your credit history and credit score, rental history, proof of income (W-2, pay stubs, or tax returns if you work a cash or contract job), past landlord and personal references, and your social security number. Proof of vehicle insurance and registration. Credit report.

Prospective guests apply through Airbnb to rent your apartment at a rate you set, sign the contract, pay their deposit, and move in – for a few days, weeks, or months. Short-term rental sites like Airbnb typically offer insurance that you’ll want to take advantage of if you are allowed to arbitrage your apartment.

Define the purpose of your event This can range from attracting a specific number of customers to your store to converting prospects into loyal customers. Ensure adequate insurance. Once an agreement is reached, ensure all terms are laid out in a written contract. Guarantee technical support. Document everything.

Insurance Policy. Snead says insurance coverage minimums are also not regulated federally, but rather by local jurisdictions. Overly cautious planners should be allowed to personally see the vehicle before signing a contract. In most cases, livery companies carry the lowest policy required by law. Drug and alcohol screening.

Typical landlord expenses can include: Landlord insurance. Buy landlord insurance. Landlord insurance protects you and your property from certain losses and accidents. Insurance also protects your financial assets if there’s a liability claim. Contracting and scheduling repairs. Create a budget. Vacancy time.

This application helps them screen prospective tenants to determine an applicant’s creditworthiness, track record, the financial capacity to pay their bills, job stability, and general responsibility level. Vehicle registration and proof of insurance. There are pets that insurance companies don’t accept for insured properties.

Call your homeowner’s insurance company. How you use your home can affect your home insurance policy. Make sure to discuss any rental plans with your insurance agent or another representative. The more privacy you can offer prospective tenants, the better.

Homeowner’s insurance records These documents can be helpful if buyers want to get a ballpark idea of the cost to insure the property. But more importantly, its a good idea to touch base with your home insurer to make sure you wont have a gap in coverage between selling your home and buying your next property.

We organize all of the trending information in your field so you don't have to. Join 10,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content